What does card not supported decline code mean?

A card not supported decline in Stripe refers to a situation where a payment attempt is declined due to a card type restriction, geographic limitations, unsupported card brand, or bank policies.

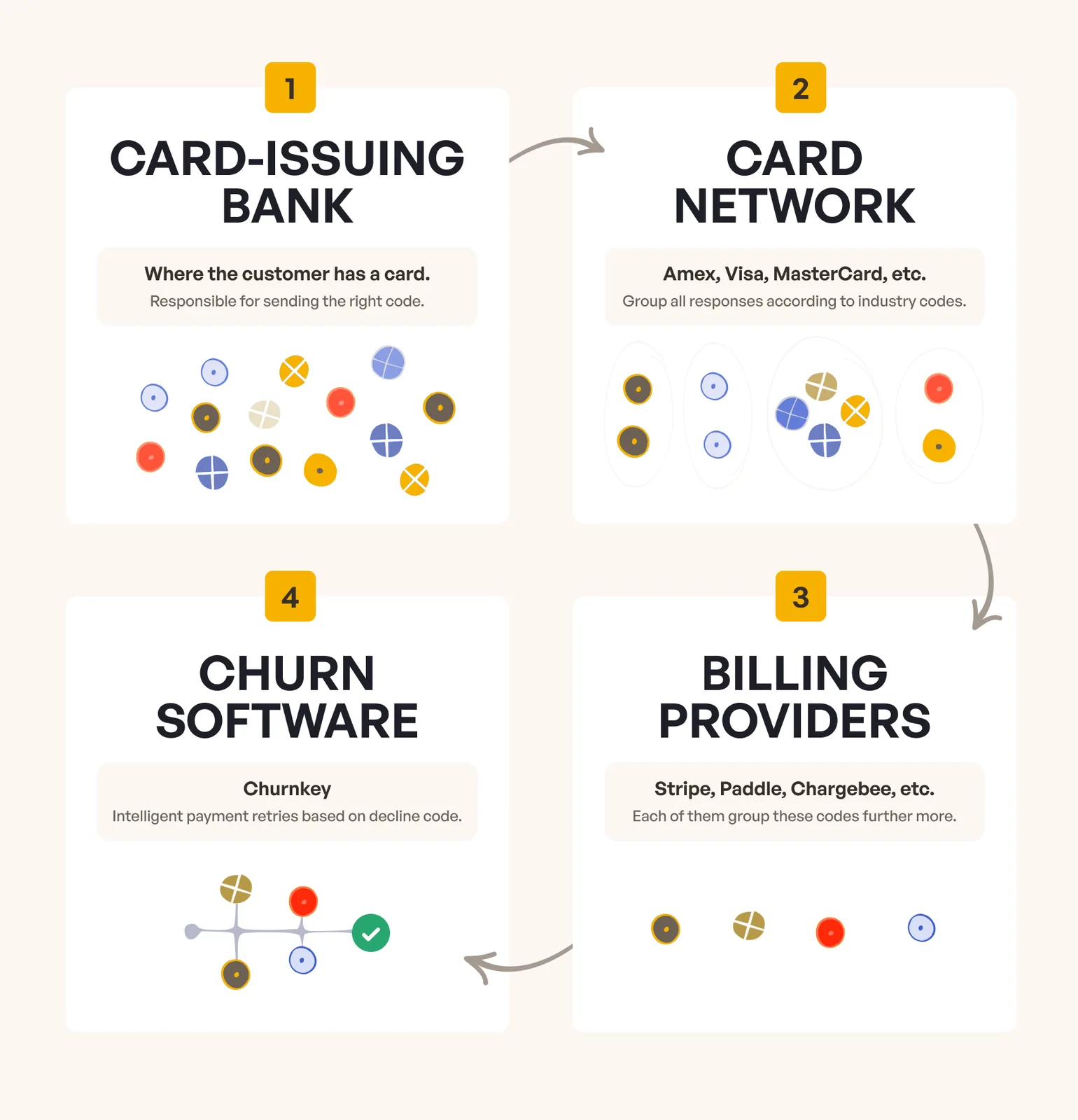

The decline code originates from the card issuing bank and is further grouped by card networks. Stripe, Paddle, Braintree further group these codes and return a code to you.

Common reasons for card not supported decline error

Common reasons for a "Card Not Supported" decline error typically relate to restrictions imposed by the card issuer.

Card Type Restrictions: The card may not be accepted by Stripe for certain types of transactions. For example, some cards may only support one-time purchases and not subscriptions.

Health Savings Account Cards, Corporate Cards, and Flexible Spending Account Cards might all come with limitations.

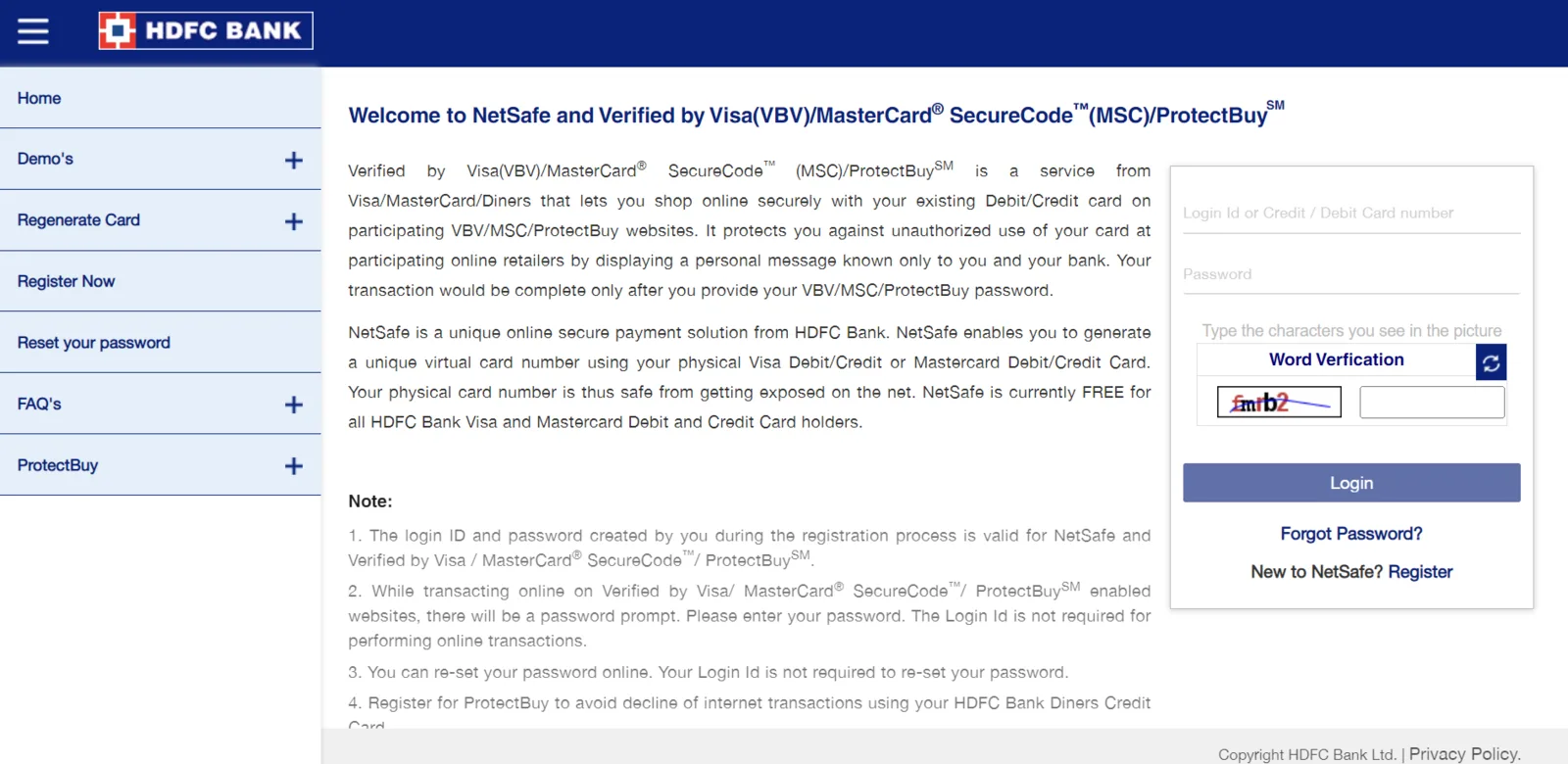

HDFC Bank would let customers set up unlimited virtual cards with a certain transaction limit. Sometimes, these cards would pass and sometimes they wouldn't.

Geographic Limitations: The issuing bank may not allow transactions from certain countries or regions. If the cardholder's country is not supported by the seller's bank or if there are cross-border restrictions.

Unsupported Card Brand: While Stripe accepts a wide variety of card types, some merchants may have configurations that limit accepted brands to major ones like Visa, MasterCard, and American Express via Stripe Radar. If a less common card brand is used, it might trigger this error.

Bank Policies: The customer's bank might have specific policies that block certain types of transactions, such as international purchases or specific merchant categories. This can also include debit cards that require a PIN for online transactions.

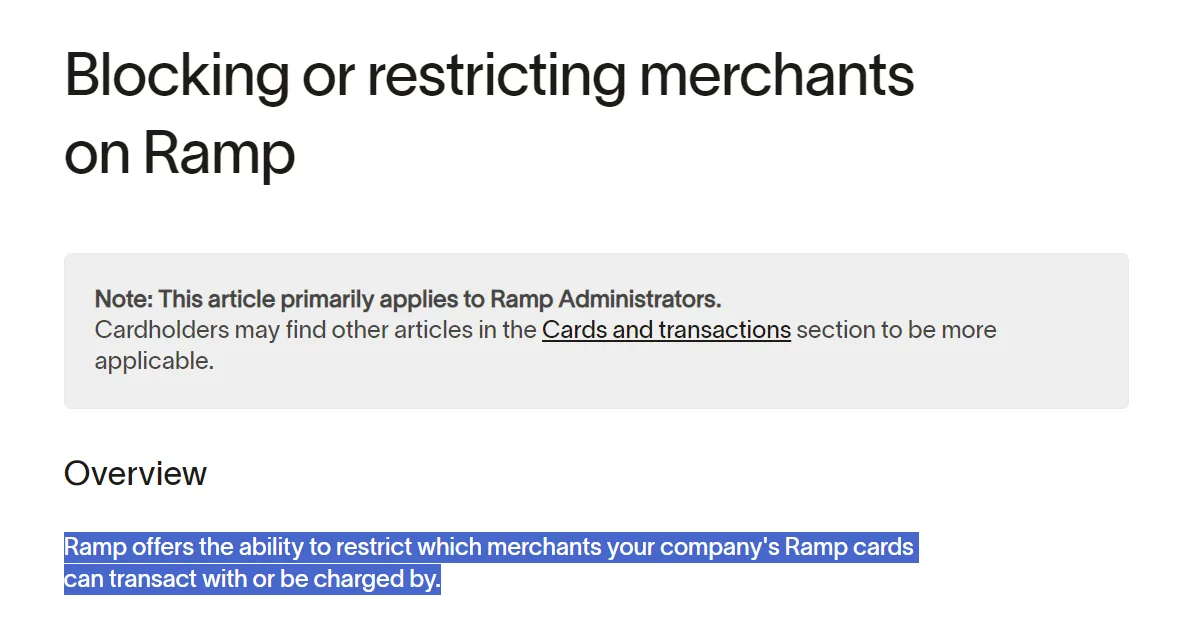

Some cards, such as corporate cards or Flexible Spending Account cards, can only be used for certain business categories such as travel or healthcare. Corporate cards can even restrict certain merchants individually or entire categories all at once.

Ramp's guide around blocking merchants and categories.

Fampay lets parents create a card for their teens. This card is sure to have some restrictions.

Card not supported decline is rarer

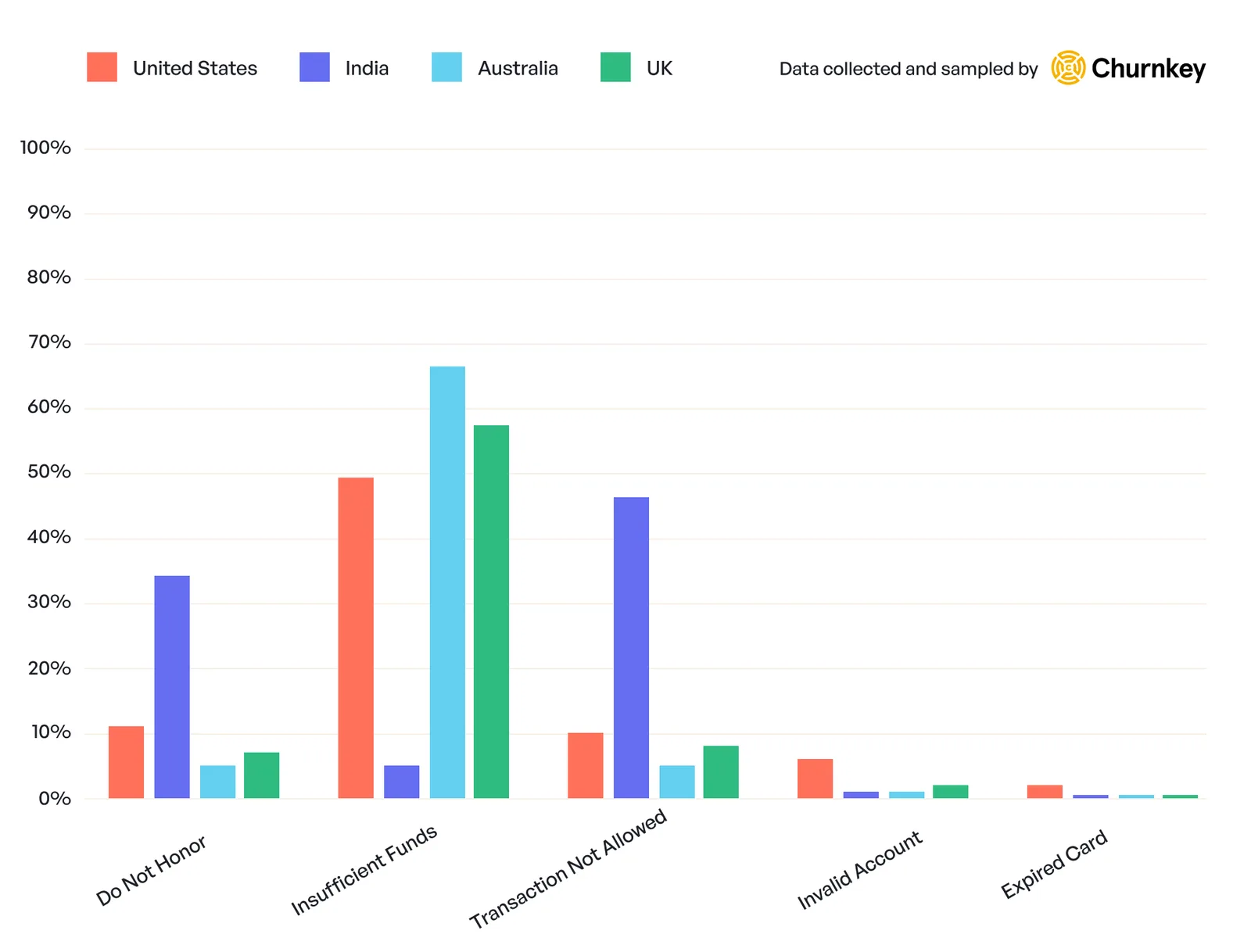

There are efforts made by Visa, Mastercard, and other card networks to encourage more specific decline codes which would help merchants and customers resolve errors faster. There's been a steady improvement over the years. Most banks return useful codes but depending on which geographical region you serve, it may vary.

As you can see, card not supported decline is not in the top 5 decline codes we see often.

Churnkey is a powerful churn software. We help companies save 20-40% of the revenue that they would have otherwise lost to churn. When you lose revenue due to a failed payment, we have four products that tackle it:

- Churn Metrics (Free): Get a free, visual analysis of your churn, especially the breakdown between involuntary and voluntary churn. This will help guide your churn reduction strategy.

- Reactivations: Reactivations target lost customers with relevant offers.

- Precision Retries: Precision Retries intelligently retry cards well within the limits and can be layered on top of Stripe's smart retries for maximum revenue boost. Precision Retries integrate natively with Stripe. Implementing it requires no code. Card Not Supported is treated as a hard decline and we don't retry this particular decline code.

- Dunning Campaigns: Dunning campaigns allow for a personalized, one-click payment recovery. For example, say you want people to update their cards? If Precision Retries can't recover the payment, Dunning will pick up where it left off. You can even customize it based on whether a failed payment is due to a soft or a hard decline.

Churnkey is also SOC-2 compliant and has robust security protocols to keep your data secured. We protect over $2B in revenue across our portfolio of companies.

To get started, sign up for Churnkey or book a demo.

Types of card not supported declines

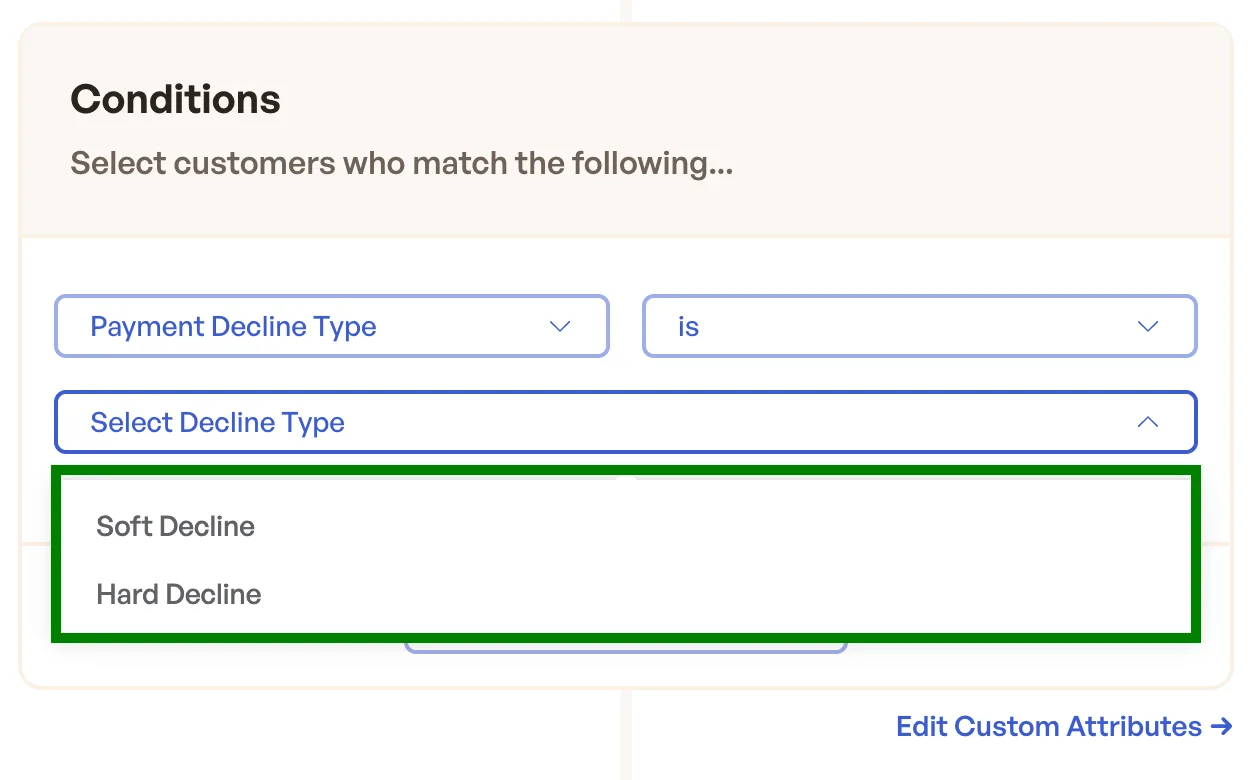

Declines can be categorized into two main types:

- Soft Declines: Soft declines are temporary restrictions. They can sometimes be resolved by retrying the transaction.

- Hard Declines: If the customer's card is not supported, they have no other option to enter a different card to continue using your service. No amount of retrying in that month will resolve the issue. You need to intervene via dunning campaigns, failed payment walls, and one-click recovery.

Learn more about types of declines:

Hard vs Soft Declines: Definition, Calculator, Strategies

How to fix card not supported declines?

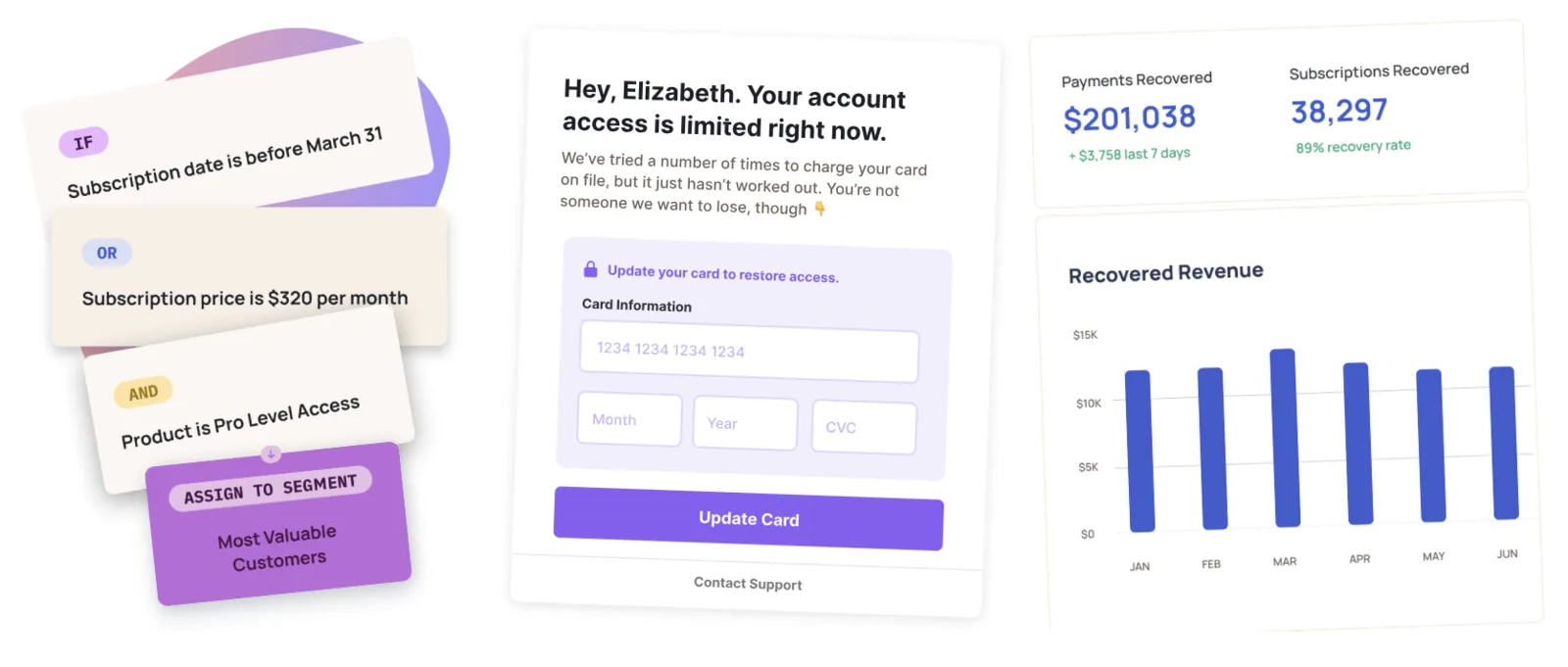

Even with all the ambiguity around the Card Not Supported Decline code, there are multiple ways to manage it if you're a subscription business. Churnkey recovers up to 89% of the failed payments with its failed payment suite of products.

1. Request card change

Context: Address these cards by asking customers to enter a different card. This requires customer action but is most likely to succeed simply because a new card is added in.

Caution: Ensure the process is seamless with no logins or multi-step verifications. Make sure the design and copy is customized to your brand.

Solution: Churnkey provides a frictionless dunning (email + SMS) platform that allows customers to update their cards easily, with options for advanced personalization (plan name, subscription age, trialing, etc.). You can also send emails via different senders to optimize for action.

To get started, sign up for Churnkey or book a demo.

2. Leverage offers and partial payments

Context: Sometimes customers will quietly let their cards decline on purpose. Offer discounts and partial payments that auto-apply to their account.

Caution: Manage potential system abuse when offering discounts.

Solution: Implement Churnkey's Dunning Offers to entice customers to update their cards with incentives like partial payments or automatic discount codes. Churnkey has anti-abuse built in.

3. Feature blocking

Context: Blocked product access can prompt action. Users can escalate this issue to their billing manager.

Caution: Prevent unpaid usage when doing so. Depending on your settings, users may be prevented from accessing certain features.

Solution: With Churnkey, you can dynamically block feature access for past-due accounts. And customers can update their payment details directly inline without navigating elsewhere. You can also decide whether to let users use the product or not.

To get started, sign up for Churnkey or book a demo.

4. Monitor metrics

Context: Since decline codes are confusing, what you can rely on are metrics. Try different offers and keep a close eye on the metrics to see what changes. Is voluntary churn higher than involuntary churn? Is there a certain decline code surfacing higher than others? Is there a certain card type that declines more than others? Use metrics to gauge the effectiveness of your retention strategies.

Solution: You don’t have time to parse overloaded charts and confusing terminology. Churnkey’s best-in-class analytics speak plainly—helping you and your team track boosted revenue, offer uptake, recovery rates, and more. You can reach out to our support team for benchmarks.

Case studies

1. Veed.io

Veed.io successfully leveraged tailored discounts and pause options, saving nearly 5,000 canceling customers. Utilizing Churnkey's Precision Retries and Dunning Offers, they recovered over 14,000 failed payments, achieving a 35% increase in their save rate. Read Veed.io's case study.

2. Sudowrite

Sudowrite boosted revenue by over six figures within a year across various churn channels by integrating Churnkey voluntary and involuntary suite into their operations. Read Sudowrite's case study.

Common errors and misconceptions with card not supported decline

Common errors or misconceptions when dealing with the card_not_supported code include:

- Retrying the transaction repeatedly: This can trigger alerts and further declines. Mastercard allows 35 attempts and Visa 15 within 30 days. Exceeding these limits can lead to fines as high as $15,000. It’s better to stay under the limits, contact the card issuer, or use a different payment method.

- Blaming the merchant: Customers often think the issue is with the merchant, but it can also be due to the card issuer's policies.

- Ignoring the need to contact the bank: Some users don’t realize that contacting their bank can resolve the issue, especially if it's due to security concerns or a need for additional verification. Although, this is a very manual process for both the customers and the merchants. You're better off automating it with Churnkey if AOVs aren't very high.

FAQs

What does card_not_supported mean on credit card?

Card Not Supported Decline is a code used by banks to indicate card type restrictions, geographic limitations, unsupported card brands, or bank policies that caused the decline. The customer should contact their bank to understand why their payment was rejected. You can also use optimized dunning campaigns, implement feature blocking, and leverage other involuntary churn reduction features.

What does card not supported decline error exceeded mean?

Typically, card not supported decline error refers to a declined transaction when the bank or the card issuing network (Visa, Mastercard) rejects a payment because the customer's card has a certain restriction (type, geographic, or bank policy) that does not allow them to transact. Stripe recommends asking users to contact the bank but there are lots of ways to reduce this decline error.